Depending on your age, you may well remember “layaway.”

It was a system that allowed you to pay for your shopping over a few installments, rather than shoving a load of cash down in one go.

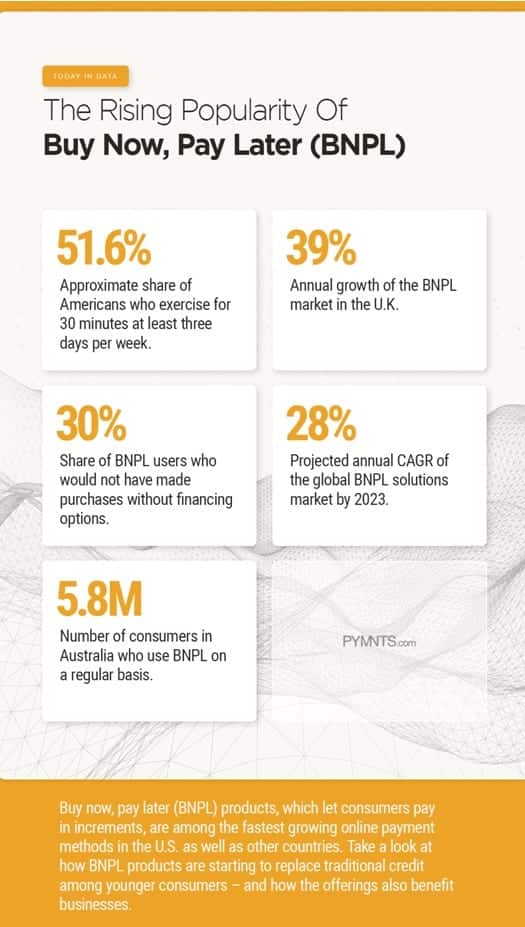

Well, this has found its way into the digital consumer world, and boy does it seem to be popular!

For those of you who have no idea what we’re talking about, we’re going to get into the what, why, who, and how, right now!

What is digital layaway?

Back in the day (we’re talking super far back in the 1920s and 1930s), layaway came into being to help people buy vacuum cleaners, cars, radios, and other larger purchases.

With this system, you would pay over a few months and after you paid the full amount, you would own your items.

This, most people would say, was sensible.

However, companies have sprung up (mainly in the United States but the technology has migrated toward Europe as well) that turned this old-time convention on its head.

Instead of waiting for your items, digital layaway plans allow you to get your items immediately but pay at a later date. Yup, instant gratification. Could this world be any more fast-paced?

These buy-now-pay-later (BNPL) apps and platform sare essentially lenders providing consumers with “online loans”. But they often target shoppers who may not be able to afford their total purchase.

These “payment can wait, your new look can’t” schemes tend to pop up when you least expect it — at the checkout. This prompts consumers to add more to their cart since they’re paying for it in “interest-free installments”.

What’s all this “interest-free” business?

Many people believe that these digital layaway companies are just outright lying about this. But they aren’t.

Generally speaking, these buy-now-pay-later systems are interest-free. However, their late fees can range from $7 to $10. One company,Afterpay, was remanded a few years ago since a large chunk of its income came from these extortionate late fees that kept adding up.

That’s right; there wasn’t a cap.

(Of course, they quickly added one after the criticism they received).

After all of this, you’re probably wondering why on earth they’re popular, right? It seems that these digital layaways can put you in some pretty sticky financial situations. Well, let’s get into that.

Why are digital layaway plans so popular?

We have one word for you—millennials. Yes, we are generalizing here. However, market research concludes that not only are millennials the main group that’s targeted for these payment plans, but they’re also the main consumer group that buys into them.

Stores primarily loved by those in the aforementioned generation such as Free People, Urban Outfitters, and Anthropologie began implementing these buy-now-pay-later plans. As we mentioned earlier, they would pop up just as people were checking out.

Research has shown that Afterpay was the preferred system here. But others such as Affirm, Klarna, and BillMeLater were used by fashion stores like MissGuided and supermarkets like Walmart.

Each of these companies has its own set of terms and conditions, but, since Afterpay, is the most popular one in the United States of America, we’ll look deeper into this company.

To use Afterpay, your basked needs to total at least $35 (capped at $1,000). When you reach the checkout, you click “Afterpay” as the payment method.

If you were a new user, you’d have to make an account and type in your payment card information into the Afterpay system.

Your cart total would be split up into four equal installments. The first one would need to be made immediately and the rest will be taken out of your bank account every two weeks. If you didn’t have the money in your account, you’d pay an $8 late fee until it capped at 25% of your order total.

These systems flooded the online fashion retail landscape at the perfect time for millennials. This generation has begun to use credit cards less, opting for alternative financing methods instead.

Why is this happening?

Student debt. Back in 2015, around 41% of this generation were drowning under student loan debt. Therefore, their credit card usage went down since it was dragging their credit scores into the mud.

Sadly, this feeling of wanting something but not being able to afford it is particularly strong in this group of consumers. Thus, they turned to creative financial plans offered by Klarna, Afterpay, and BillMeLater to get their hands on the things.

Now for the biggest question…

Will this consumer trend continue?

This consumer trend is pretty addicting. These loans are made to be enticing—and it works.

The companies don’t check your credit score or income to see if you can actually afford to pay it back every two weeks. Thus, it’s up to the consumer (you) to be sensible. However, it’s easy to get sucked into the spiral of “oh, I’ll just pay it off later” which inevitably turns into debt.

So, what’s going to happen to this trend? This is, perhaps, one of the biggest questions financial experts have about digital layaways.

In our opinion, yes, this trend will continue to grow. The “necessity” for instant gratification seems to be consuming the entire world at this point (mostly generation Z and millennials).

While no one can say for sure, more people will likely get sucked into these buy-now-pay-later payment schemes.

If you can afford to pay it back on time, this isn’t such a bad thing. However, people who work on instant-gratification mode tend to be younger, earn less, and therefore, less likely to pay it off promptly.

But, it’s not all doom and gloom!

With all of that being said, buy-now-pay-later plans aren’t all doom and gloom. There are times when putting down a small deposit to bag yourself an item for later payment can be a good thing.

Here’s where it can come in handy:

For budgeting

If having a monthly repayment plan will allow you to make smarter budgeting decisions (and you have the discipline to do it), there’s nothing wrong with paying later.

High demand, short supply

If an item won’t be around when you can afford it outright, then paying for a quarter of it initially and the rest later might be a good way to go.

When you need it

Using digital layaway when you don’t need an item can create terrible habits that get you into the loop of living above your means. However, if you urgently need an item but won’t have the money to afford it until next month, paying later can help.

The bottom line

While there is no need for them on a whim since you should be spending less than you make, the rise of digital layaway could be helpful in times of need.

Whether millennials will learn to use them this way, however, remains to be seen.

- 9 Essential Aspects of Your Brand Identity

- Everything You Need to Know About Prototyping for Small Businesses

- Food Metal Detection Testing Procedures

- 5 Strategies to Increase B2B Wholesale Sales

- The Comparison Between Crowdfunding and Peer to Peer Lending

- Beyond the Hype: Former AT&T and Synchronoss CEO Glenn Lurie on What the $4 Billion GenAI Telecom Market Really Means for 2025