Any business requires financial accounting. If you don’t have it, then you don’t know answers to the crucial questions. How much money do you spend and why? The sale of which goods/services brings you more profit? What if your business is unprofitable at all? The constant and detailed accounting of income and expenses isn’t a simple task. It means a significant investment of time and attention in creating a profit and loss statement. So, it requires the owner’s efforts or involvement of accountants and analysts.

In this article, we will talk about what is a profit and loss statement and look at some examples. Let’s consider different options of automation, their pros, and cons. You will see the costs of creating IT solutions for small businesses. As a result, you will be able to make the right decision for your company.

Why is small business accounting automation important?

Modern technologies allow completing various routine tasks without great efforts. You can organize accounting for different documents with the help of machines. This approach allows almost totally automate your business daily processes. In addition, the automation reduces the risk of errors caused by human factor. This is especially true for small businesses. Because the owner often has to keep financial records independently without having a deep knowledge of this sphere.

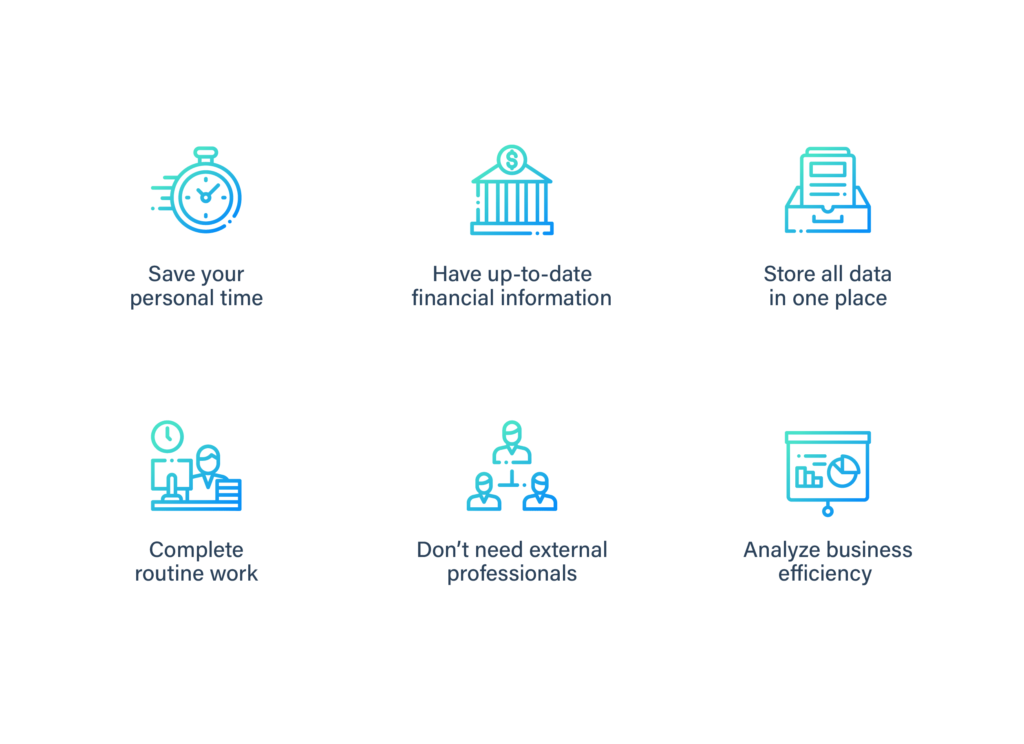

What are the benefits of business automation?

- Saving your personal time and the ability to complete other tasks.

- Easy access to up-to-date financial information.

- Storing all data in one place.

- Significant time savings on performing routine work.

- Reducing the cost of turning to external professionals.

- The possibility to analyze the profitability of your business.

However, these are not all the benefits of small business automation. Read more in the article on how to reduce SMB expenses by workflow automation.

Profit and Loss Statement for small business

A clear understanding of business efficiency requires the creation of a profit and loss statement. The simplified version of this report contains information on:

- your income (revenue) from the sale of goods/services

- your costs for the producing and distributing of goods/services

- the difference between revenues and costs

To clarify, the variance between income and cost is your profit. If the value is negative, it’s a loss.

What does P&L statement consist of?

An income is the sum of money you get for selling a product or service. Costs are the money you pay to suppliers and employees for the production of goods/services.

Costs usually have some peculiarities. For example, there are variable and fixed costs.

Variable costs are those that the company invests directly on the production/sale of goods/services. For example, the cost of:

- delivery of goods

- purchasing raw materials

Fixed costs are those that a company has regardless of whether it sells goods/services or not. For example, the cost of:

- energy supplies in the office

- office or warehouse rental

- taxes

- loan payments (if they were taken for business needs)

The next profit loss statement feature is the time period covered by the report. Usually, there are two types of the document:

- report for a month, quarter, half-year or year

- report within a specific project

The first one usually includes indicators for the same period of the previous year. So, you can compare and check business performance. This approach provides an opportunity to further analyze the dynamics of company development. You will also see the growth of income and expenses in certain categories.

Project P&L is quite like project costing. It shows how much profit the company receives from the implementation of a specific service or product. Such a P&L statement shows which projects are more profitable. The business owner can see which stage of implementation is the most expensive. It also helps to predict the costs of similar projects realization in the future.

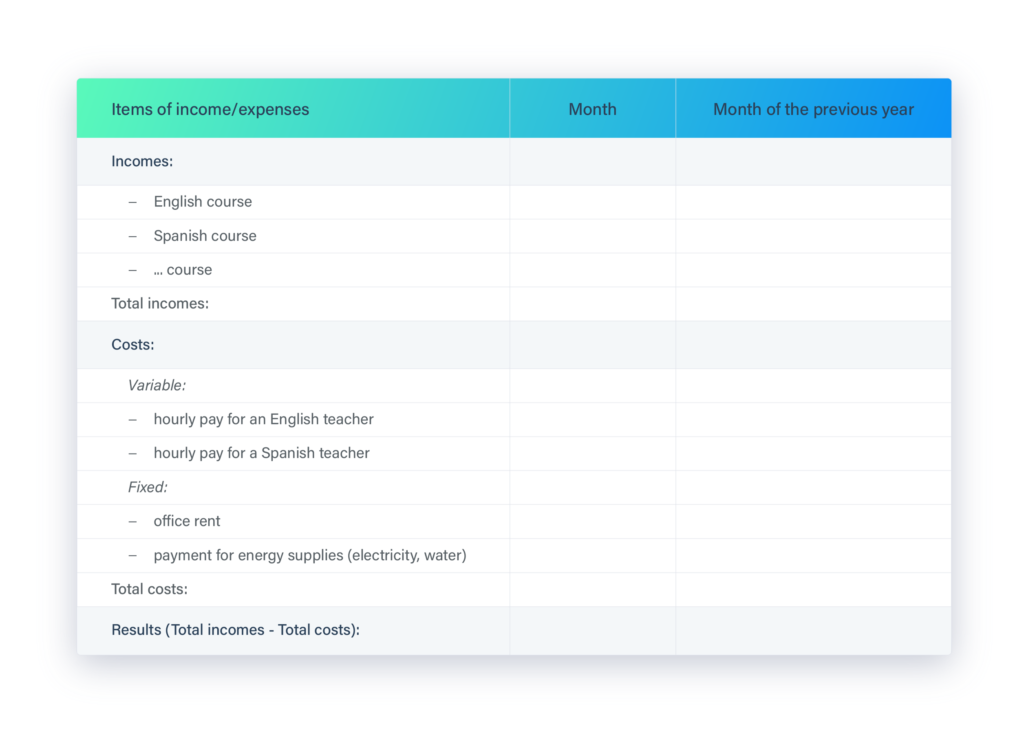

P&L statement for certain periods of time

This document contains information on income and expenses during the reporting period. For example, let’s look at a template of a simple financial statement. The time interval is one month. The income includes all sales of goods/services that have been implemented during the month. Most importantly, you should be mindful of categories that bring your income. They depend on the specialization of your business. It’s also necessary to divide them into fixed and variable costs.

Here’s the simplest report for small business that provides educational services:

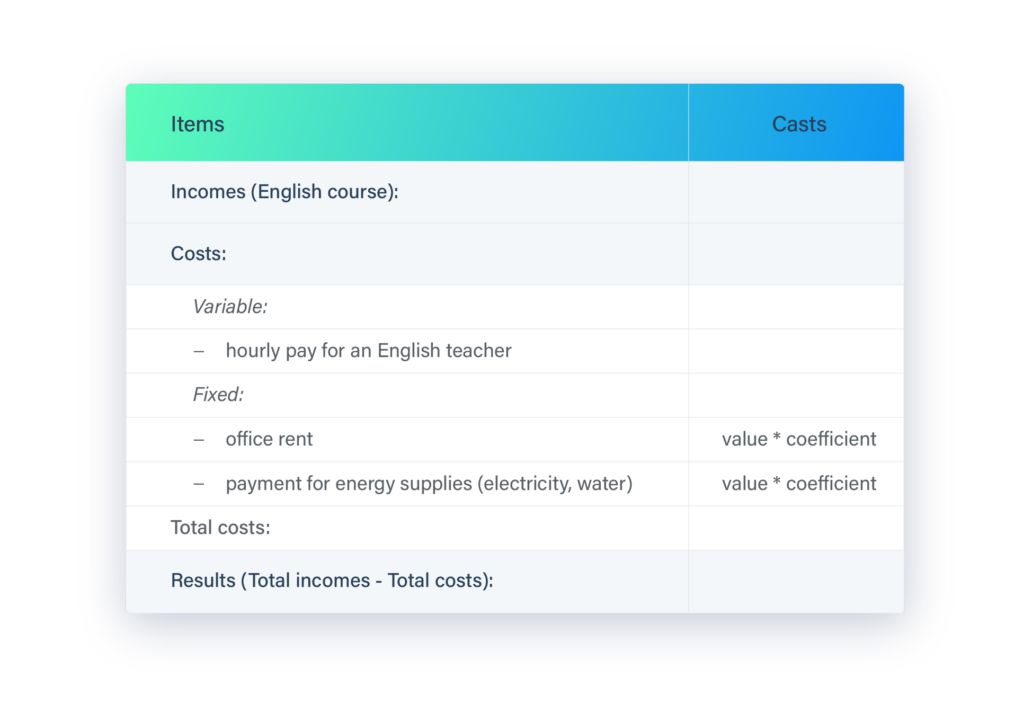

Project P&L statement

It’s a single report on all incomes and expenses on a project for the whole period of its implementation. Therefore, revenues include all sales of goods/services completed under the project. At the same time, you can see all the costs associated with it. As for the description of fixed costs, it’s difficult to determine them for a specific project. However, it’s still necessary to check the fixed costs. So, you should denote the proportion of revenue for the implementation period. The formula is revenue received from the project divided by the company’s total revenue for the time spent on the project. Then, the fixed costs at the period implementation are multiplied by the coefficient of the proportion.

For example, look at the simple project P&L statement:

If the company provides a similar service regularly, then we can analyze its effectiveness. But the parameters for analysis are another topic.

Automation of P&L statement

Profit and loss report gives the company a wide space for analyzing business performance. So, you can understand which parts of the company are working better, and which should be improved. Therefore, continuous P&L management requires a lot of time. It also causes the involvement of qualified professionals. As a result, it leads to significant costs for small businesses.

The process of creating a P&L statement can be almost completely automated. There are several ways to achieve this. For example:

- introduce in the company of ready-made small business accounting services

- create P&L statement as separate tables in Excel or other tabular applications

- develop a unique accounting system for a specific company

So, let’s look at the pros and cons of these 3 options for creating P&L statements.

Option 1: ready-made software

First of all, using ready-made solutions can be challenging. That is to say, the available programs don’t always take into account all the characteristics of a particular company. So, they often require customization and modernization for specific purposes. In addition, most of the existing systems are too bulky for small businesses. So, sometimes it’s easier to use Excel tables instead of implementing complex solutions.

However, actively growing companies that sell a lot of products/services can use ready-made solutions. Because the programs are designed for businesses that deal with dozens of suppliers and have more than 300 specialists.

Option 2: Excel

Secondly, separate tables in Excel allow creating an accounting system for specific processes. So, it’s a reasonable step for small companies. Moreover, you can create your own profit and loss template Excel, or find an example on the Internet. As a result, you will have several possibilities:

- Automatic generation of simple profit and loss report for various periods or projects.

- Checking the effectiveness and profitability of the business.

- Controlling all revenues and all company expenses.

On the other hand, the disadvantages of profit loss statement Excel are:

- The solution has limited functionality because the capabilities of Excel aren’t very powerful.

- With your business growths, you will need more and more time for accounting in Excel.

- Building individual applications based on Excel requires cooperation with a software development company.

Option 3: custom development

Thirdly, the development of your own accounting system. This approach is a promising choice in case of difficulties with financial accounting in Excel or Google-tables. The advantages of custom software development are:

- The system will be created directly under the company’s business processes, taking into account all its features.

- Wide possibilities of modernization P&L statement in the future as the company grows.

However, you may face some cons of such business automation solutions:

- The necessity of well-established business processes that can be automated.

- Extra costs for creating an individual accounting system and its maintenance.

To sum up, let’s consider the costs of automation solutions. Above all, you should first create an MVP (Minimum Viable Product). It performs the basic set of functions and can be developed within a budget of 10-15 thousand dollars for about 2 months.

So, the architecture of the application will provide the possibility of easily adding new functions. For example, to conduct full financial accounting within one application, to form a P&L sheet and Cash Flow. If you want to know more about business automation software, read the article on how to automate Cash Flow.

- Financial Management Essentials for Competitive Businesses

- 3 Secured Loans to Consider During a Financial Emergency

- Saving Money In Your Office And In Your Business

- Does Having More Credit Cards Give You a Better Credit Score?

- Online Stock Trading Tips for New Investors

- How Blockchain Accounting Will Completely Transform Finance