The life of an entrepreneur can be a stressful one at the best of times. So when you find yourself in the position of owning multiple businesses across various range of industries, it can make for a mighty game of plate spinning.

Spotting a market niche, researching it, and strategically providing a service that fills a gap can be hard enough – then comes the upkeep, the background knowledge, and plans for sustainability.

There’s plenty to take into account for business owners across multiple industries, so here’s a deeper look at seven key challenges that entrepreneurs in two or more sectors face – along with some tips that could help them keep their heads afloat:

1. Embrace the Struggle

It can be tremendously difficult when launching a new business in an industry that you’re not used to. The chances are that there’ll be a fresh set of regulations, unexpected operating costs, and customer wants and needs that could take you by surprise.

In an alien industry, you may find that starting with a new endeavor can be a struggle. Within this challenge lies an opportunity to gain a thorough lesson on how to survive.

If you embrace the struggle of starting, avoid hiding away or calling on others to take your problems on for you, the chances are that you’ll be able to grow your business equipped with an extensive range of knowledge and life lessons that would’ve otherwise eluded you.

2. Never Assume

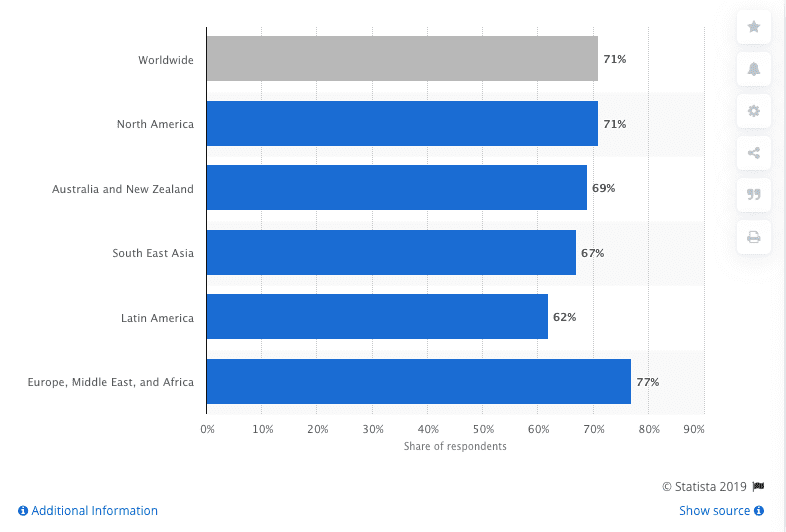

The chances are that you’ll be conducting a broad range of market research to understand your prospective customers better. In an industry that you’re not familiar with, this is an excellent way of knowing who you’re marketing to and the kind of things they would want from your product or service.

(Image showing the effectiveness of marketing in different parts of the world. Image: Statista)

However, be careful of drawing too many assumptions, even if the data appears to support your ideas. There’s always going to be an unexpected twist and turn in the road towards establishing yourself on the market. It’s important to set some resources aside for such an eventuality. For example, your initial marketing campaign could only appeal to a smaller section of your industry, or maybe you’ll underestimate the space needed to store your products. Either way, it’s best to keep braced for when an oversight occurs.

3. Source Expert Help…

It’s not always about what you know, but who you know. When entering into an alien industry, you must look to experienced peers for advice. There’s no better way of navigating the choppy waters of a new industry than by picking the brains of somebody who’s already been there and done that.

You could action this by either enrolling them into the company or only by asking to meet them to discuss the ins and outs of your new industry.

Many entrepreneurs opt to open their business up to venture capital firms, not only for the money but for the guidance of experienced professionals. Here, venture capital firms can advise you on the steps to take and even offer up a little bit of promotion and positive PR to the right audiences. Of course, enlisting the help of a venture capital firm will also likely cost you a significant portion of the equity in your business. Owners can also look to woo an angel investor, who may be able to provide some valuable insights – but are typically much rarer to find.

4. Use Your Fresh Perspective as a Strength

Yes, expert help can be essential in allowing you to grow your business strategically without any preventable setbacks, but you mustn’t let an external voice cloud your judgment too much.

There’s a reason behind why you’ve chosen to enter into a new industry – you clearly must have a vision of how to run a successful company in a different market. Never let anybody steal your idea from you under the pretense of offering up their experiences.

Fundamentally, you can gain plenty of industry insight from the help of experienced professionals, but the chances are that your business will need to be different to succeed. Be sure to maintain your fresh perspective of this new industry and utilize it within your USP. Your blue-sky approach to business could well lead to a wildly successful enterprise.

5. Keep Critical

Never take anything for granted. You’ll interact with many industry experts that will have more relevant experience than you – but this doesn’t mean that they’ll always be right.

The same goes for your market research, and focus grouping that takes place, and the cash flow forecasts you conduct. You’re in a new industry, so nothing can be considered as gospel before you see it for yourself.

Perhaps the best course of action to take here is to look at your target audience carefully and broadly. Be sure to not only craft an image of your desired customer but of other prospective customers.

Like the case of vinyl, there may be an established older audience that cherishes the traditional form of music equipment. Still, it has an unlikely growing market among Millennials and younger collectors. Be sure to look at all the customers you can potentially attract and explore how you can cater to all of them.

6. Hire Strategically

When it comes to working in a brand new industry, it’s pivotal that your recruitment policy has the right staff in mind.

Some companies like to hire locally, while others prefer to train young recruits early on in their life with the business. But as you may well be still trying to gain fluency in a new industry, it could be much more beneficial to hire workers who have bags of relevant experience from the off.

By looking to hire staff who have their industry knowledge, you can effectively bounce ideas off them and call on them to effectively train newer recruits in the future. This challenge requires a little bit of introspection, however, and it’s essential to take a look at your business and figure out what it needs in terms of recruitment strategy.

7. The Need for Revaluation

If you’re looking to thrive in a new industry, it’s essential to allocate as much time as possible into evaluating and reevaluating your goals, processes, policies, and business goals. Many markets are erratic enough in this day and age – let alone one that an entrepreneur lacks experience in.

Make sure you take the time to evaluate your business at regular intervals. There’s no time for complacency, and it’s essential to address any shortcomings as early as possible to familiarise yourself with the fresh challenges your business faces.

Being an entrepreneur that likes to dabble in multiple industries can be a daunting challenge, but isn’t that part of the excitement that can, at times, make the world of business ownership one of the most fun places to be?